Award-winning PDF software

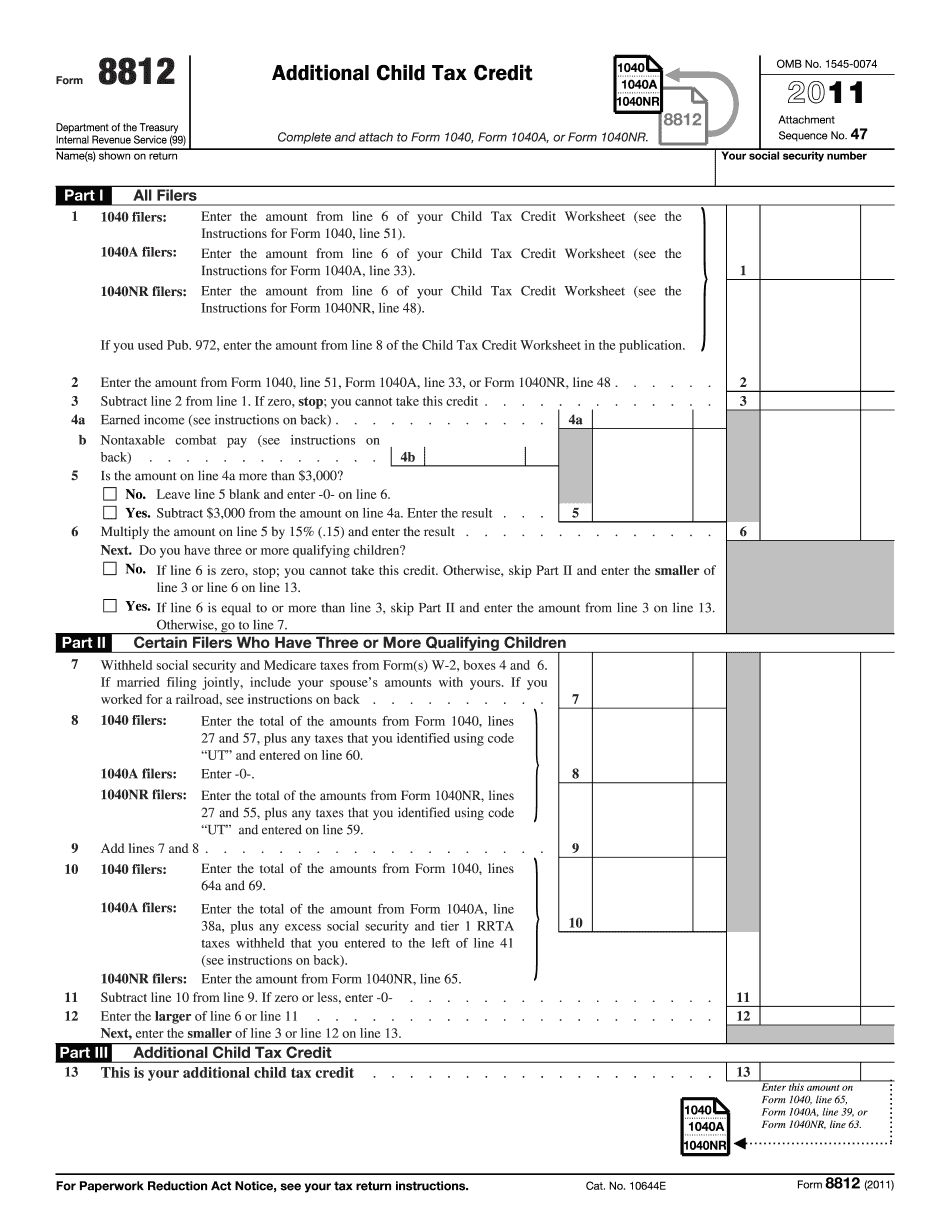

What is form schedule 8812 & filing instructions

If you are a married filing jointly, you will qualify for the 1,000 child tax credit. However, if your . . . You have earned taxable income (including interest and dividends) that's in excess of 4,050 (the maximum credit allowed) you can obtain an additional 1,000 tax credit. Therefore, if you are a married filer who earned taxable income of 10,050, and you qualify for the additional child tax credit, you will receive an additional credit of 1,000. This is true regardless of the modified adjusted gross income (MAGI) of the taxpayer. For further information see the following page which summarizes how the Credit was calculated. “Tax Credit for Unmarried Pregnant Women” . . . You can find a summary of the new credit calculation for child tax credits on page 11 of the Publication 970, Tax Guide for Individuals (2015 edition), published by the Internal Revenue Service. “Childcare Credit for Parents” . . . There.

What is the form 8812?

Nov 4, 2021 — If you paid less than 200 when you file your 2016 return, you can claim the 150 of ETC for a dependent who is not part of your family. Nov 5, 2021 — You may have to pay more than 400 to file your 2017 return if you claim the Earned Income Tax Credit to support a dependent child. Nov 5, 2021 — If you paid more than 3,000 to claim a child's exemption through the 2017 return, you might have to pay a penalty if you do so again. Nov 5, 2021 — If you are claiming a child or dependent care credit in the same return for two or more people, you can split them up between them. Nov 5, 2021 — You can report multiple dependents on Schedule A, and you do not have to split them up among them. Nov 6, 2021 — You.

Child tax credit schedule 8812 | h&r block

The earned income and . you have earned income and are not married, it's best to calculate each child's amount separately so that any combined credit you receive isn't reduced. Your deductions and credits. In 2014, the income tax rate is for married couples. The standard deduction is 6,300 (or 12,600 if married filing jointly) for individuals, or 6,750 (or 15,000 if married filing separately) for married couples filing jointly. The earned income credit is up to 1,000 (or 2,400) per qualifying child but not less than 2,000, and the child's earned income credit is up to 1,500 (or 2,800). If your child's earned income is more than one-half of the income of your family, you must calculate at least half of that earned income (if the parent of the child who isn't your qualifying child is your spouse). That earned income must be earned in the year the child is born. A child is considered a qualifying.

Federal form 8812 instructions - esmart tax

If you want all of these forms with your return, I recommend you print off and fax them to me, so we'll have them ready to go. Step I: Get your tax return from the IRS to see what is available. Here are the forms you will need. Form 1040, line 21. Form 1040EZ, line 19. Form 742 (child tax credit claim) Form 8559 (business income tax return/return of qualified business income and qualified use of personal property). Form 8800 (form 8951) Form 959 (employment tax return and return of adjusted gross income for individuals) Form 1040-SS. Form 1040-SR. If your state issues child tax credits, look to see if one is available for your household. If you don't have any state credits available, you will be able to apply them to your federal tax return. I would not bother until after you have a Form.

Schedule 8812 - additional child tax credit - taxslayer pro

PDF, each dependent can claim the full amount of the non-refundable credit for himself or herself. (The dependent must also meet the other eligibility requirements.) There are exceptions to the general rule about taking tax deductions for each qualifying child. You can, for example, treat your second child as a qualifying child if he or she would qualify as a qualifying child for one of your other children if you claim the deduction for the first child. (See the table of tax benefits at .pdf.) If you claim the other child's tax benefit on your return, it won't appear on your return as a deduction. However, the amount of that benefit is reduced over a 12-month period (called a “rolling phaseout”). If your child is not already eligible for the credit, you can request a new 1099-C. (See .pdf) for the tax year you file the return. If you already.